The value of the Coal Mine Pljevlja was overestimated by at least a third, i.e. around €12 million. Because of that, Aco Đukanović, brother of newly elected President Milo Đukanović, will earn from the sale of shares to EPCG €1.4 million more than they are really worth, while the Italian company A2A will make additional profit of almost €1 million.

The value of the Coal Mine Pljevlja was overestimated by at least a third, i.e. around €12 million. Because of that, Aco Đukanović, brother of newly elected President Milo Đukanović, will earn from the sale of shares to EPCG €1.4 million more than they are really worth, while the Italian company A2A will make additional profit of almost €1 million.

This is shown by the analysis conducted by Milenko Popović, financial consultant and professor of economic sciences, in cooperation with MANS Investigative Centre.

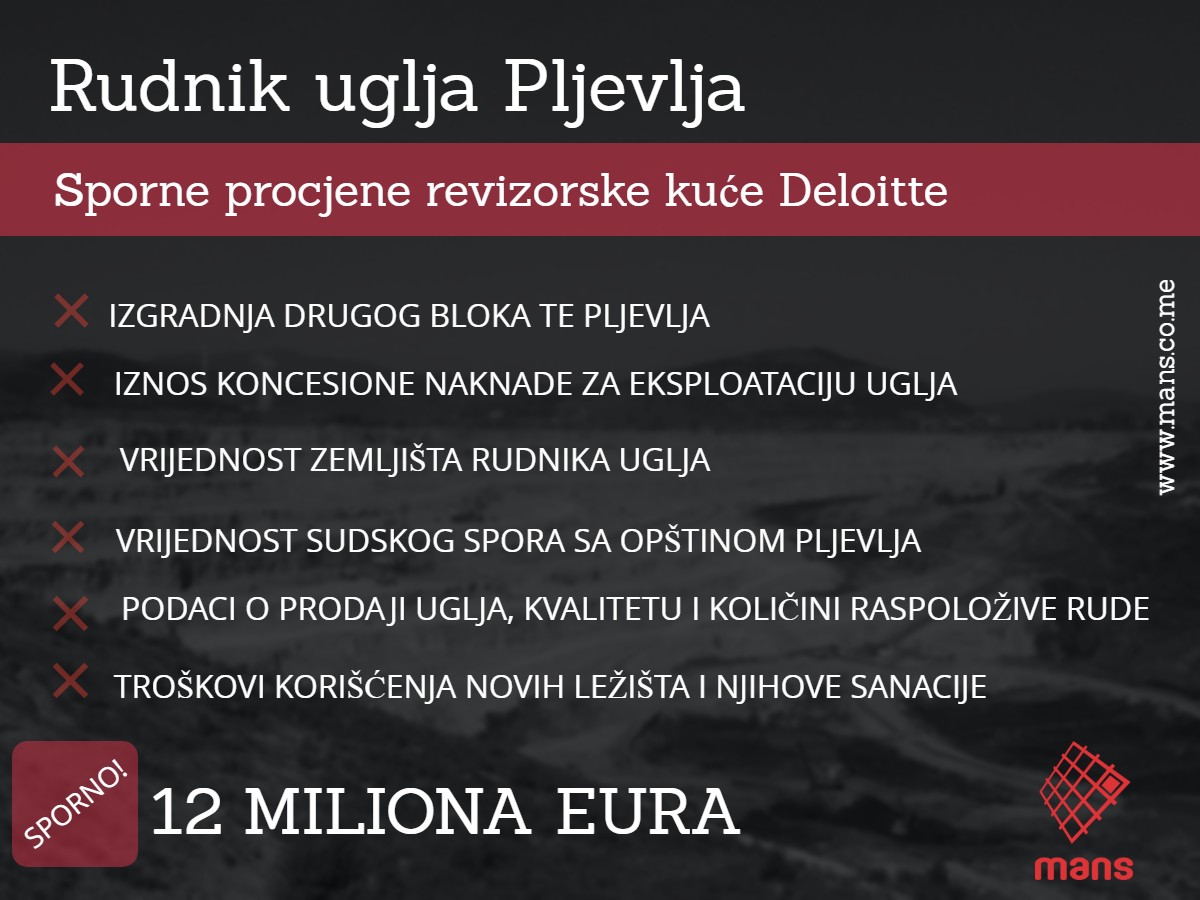

Prior to the purchase of the Coal Mine, EPCG hired audit company Deloitte which estimated that the Coal Mine was worth € 32.5 million. For this assessment, Deloitte only used data provided by the Coal Mine, whose reliability was not checked, as stated in their analysis. However, these data were based on unrealistic projections, which increased the estimated value of the Coal Mine.

Thus, the value of Pljevlja-based company depends to a large extent on the estimated potentials and future investments, primarily the construction of the Second Block of Thermal Power Plant Pljevlja. Deloitte has projected that in only four and a half years the money for construction will be found, all permits will be obtained and a new thermal power plant will be built, although only four months ago a contract with Czech Škoda was terminated because no funds were found. After the termination of the contract, EPCG pledged that by the end of January this year, the Government would propose an alternative solution, but this is yet to happen.

Postponing of implementation of the Second Block project lasting from three to five years would affect the decline in the estimated value of the Coal Mine for 3.6 to €6.6 million, the analysis of the economic expert Popović and MANS Investigative Centre shows. If the delays were greater, then the decline in company value would be higher.

In addition, Deloitte predicts that the Second Block will work by 2062, which is contrary to the European Union policy whose member states will close coal-fired power stations by 2050. If Montenegro is to enter the EU by then, it will have to close the Second Block 12 years earlier, which would further reduce the estimated value of the Coal Mine, but this was also not taken into consideration by Deloitte.

Deloitte projects that the amount of the concession fee will not change in the next 50 years, which additionally increased the estimated value of the Coal Mine. If the current concession fee increased from less than €700 thousand to million a year, then the estimated capital of the Coal Mine Pljevlja mine would decrease by more than € 3 million, the analysis of the MANS Investigative Centre shows.

Value of this company is unrealistically high due to the unrealistic assessment of the Coal Mine land. The largest part of the land owned by this company is located at the location Jagnjilo in Pljevlja, a landfill that needs to be rehabilitated. The square of such land is estimated at €1.5, while on a similar distance from the town one can buy high-quality agricultural land for only 40 cents per square meter.

Also, there is a controversial assessment of the value of the court dispute with the Municipality of Pljevlja in the amount of 5€ million, which refers to the contract on the planning of construction land. Instead of reducing the value of the Coal Mine for the entire amount, Deloitte reduced the capital of the company by only two million, referring to the management’s assessment that the probability of losing the dispute was 40%. At the beginning of 2015, the Commercial Court in Bijelo Polje rejected the lawsuit of the Municipality, but the Appellate Court abolished the verdict and returned the case to retrial.

In assessing the value of the Coal Mine, Deloitte does not give an explanation as to how the mine ended the previous year with an unusually high cash amount of €6.1 million. Director of the Coal Mine, Slavoljub Popadić, claims that this is due to the company’s good business in the past year. “We repaid earlier loans, we have been granted the reprogram of the tax debt, we sold more coal in Serbia and Kosovo, and invested less in capital investments,” Popadić explains.

The Coal Mine ended previous years with much less cash, from around €25 thousand in 2010 to less than €337 thousand in 2016, while at the end of last year it had 18 times more cash. However, Deloitte assessed the value of the Coal Mine only on the basis of an extreme cash surge in last year, not taking into account the company’s average business in the previous period.

According to the same principle, Deloitte used only data on unusually high sales of coal in the previous year. In addition, the estimate is based on unrealistic data on the quality and quantity of available ore, and it does not include the costs of using new bearings and their subsequent remediation.

Deloitte itself noted that in its evaluation they did not check the data on which they based their conclusions, and at the same time disassociated themselves from their own findings. “If the plans and assumptions used are not realized for any reason, this can affect the conclusions presented and such impact can be materially significant.”

However, Deloitte’s assessment which increased value of the Coal Mine for at least €12 million has also “inflated” the value of shares from €4 to €6.4.

Direct consequence of such assessment is benefit for the shareholders of the Coal Mine who will charge their shares more expensively at the expense of EPCG, whose business ventures are paid by the citizens through electricity bills.

Thus, A2A will collect an additional €5 million, while Aco Đukanović, one of the largest shareholders of the Coal Mine, will receive from EPCG €1.4 million more than its shares are really worth.

Ines Mrdović, MANS Investigative Centre

{kind=link}